Real Estate Tax Credits and Grants

Minimum Expenditure Requirements for Historic Rehabilitations

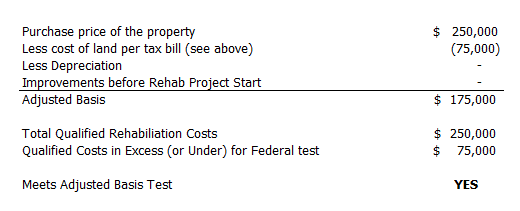

Federal requirements

The National Park Service states that “substantial rehabilitation test….this means that the cost of rehabilitation must exceed the pre-rehabilitation adjusted basis of the building. Generally, this test must be met within two years or within five years for a project completed in multiple phases. A – B – C + D = adjusted basis [A = purchase price of the property (building and land); B = the cost of the land at the time of purchase; C = depreciation taken for an income-producing property; D = cost of any capital improvements made since purchase].”

Compliance is calculated as follows:

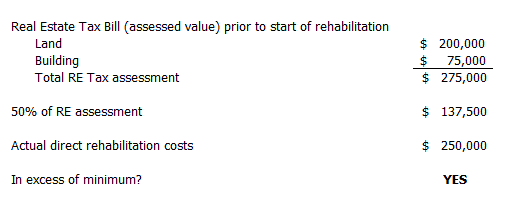

Commonwealth of Virginia Requirements

Virginia Department of Historic Resources, Historic Rehabilitation Tax Credit Regulations state: 17 VAC 10-30-120. Qualification for credit. Material rehabilitation means improvements or reconstruction consistent with the standards for rehabilitation, the cost of which amounts to at least 50% of the assessed value of the buildings for local real estate tax purposes for the year before the start of rehabilitation. Compliance is calculated as follows: